Appendix to Subpart H—Calibrating the GSIB Surcharge*

Abstract

This white paper discusses how to calibrate a capital

surcharge that tracks the systemic footprint of a global systemically

important bank holding company (GSIB). There is no widely accepted

calibration methodology for determining such a surcharge. The white

paper focuses on the “expected impact” framework, which is based on

each GSIB’s expected impact on the financial system, understood as

the harm it would cause to the financial system were it to fail multiplied

by the probability that it will fail. Because a GSIB’s failure would

cause more harm than the failure of a non-GSIB, a GSIB should hold

enough capital to lower its probability of failure so that its expected

impact is approximately equal to that of a non-GSIB.

Applying the expected impact framework requires

several elements. First, it requires a method for measuring the relative

harm that a given banking firm’s failure would cause to the financial

system—that is, its systemic footprint. This white paper uses the

two methods as set forth in the GSIB surcharge rule to quantify a

firm’s systemic impact. Those methods look to attributes of a firm

that are drivers of its systemic importance, such as size, interconnectedness,

and cross-border activity. Both methodologies use the most recent

data available, and firms’ scores will change over time as their systemic

footprints change. Second, the expected impact framework requires

a means of estimating the probability that a firm with a given level

of capital will fail. This white paper estimates that relationship

using historical data on the probability that a large U.S. banking

firm will experience losses of various sizes. Third, the expected

impact framework requires the choice of a “reference” bank holding

company: A large, non-GSIB banking firm whose failure would not pose

an outsized risk to the financial system. This white paper discusses

several plausible choices of reference BHC.

With these elements, it is possible to estimate a capital

surcharge that would reduce a GSIB’s expected impact to that of a

non-GSIB reference BHC. For each choice of reference BHC, the white

paper provides the ranges of reasonable surcharges for each U.S. GSIB.

Introduction

The Dodd-Frank Wall Street Reform and Consumer Protection Act1 mandates

that the Board of Governors of the Federal Reserve System adopt, among

other prudential measures, enhanced capital standards to mitigate

the risk posed to financial stability by systemically important financial

institutions (SIFIs). The Board has already implemented a number of

measures designed to strengthen firms’ capital positions in a manner

consistent with the Dodd-Frank Act’s requirement that such measures

increase in stringency based on the systemic importance of the firm.

As part of this process, the Board has proposed a set

of capital surcharges to be applied to the eight U.S. bank holding

companies (BHCs) of the greatest systemic importance, which have been

denominated global systemically important bank holding companies (GSIBs).

Setting such an enhanced capital standard entails (1) measuring the

risk that a given GSIB’s failure poses to financial stability (that

is, the GSIB’s systemic footprint) and (2) estimating how much

additional capital is needed to mitigate the systemic risk posed by

a firm with a given systemic footprint.

This white paper explains the calibration of the capital

surcharges, based on the measures of each GSIB’s systemic footprint

derived from the two methods described in the GSIB surcharge final

rule and discussed in detail in the preamble to the rule. Because

there is no single widely accepted framework for calibrating a GSIB

surcharge, the Board considered several potential approaches. This

paper focuses on the “expected impact” framework, which is the most

appropriate approach for helping to scale the level of a capital surcharge.

This paper explains the expected impact framework in detail. It provides

surcharge calibrations resulting from that framework under a range

of plausible assumptions, incorporating the uncertainty that is inherent

in the study of rare events such as systemic banking failures. This

paper also discusses, at a high level, two alternative calibration

frameworks, and it explains why neither seemed as useful as a framework

for the calibration of the GSIB surcharge.

Background

The failures and

near-failures of SIFIs were key drivers of the 2007-08 financial crisis

and the resulting recession. They were also key drivers of the public-sector

response to the crisis, in which the United States government sought

to prevent SIFI failures through extraordinary measures such as the

Troubled Asset Relief Program. The experience of the crisis made clear

that the failure of a SIFI during a period of stress can do great

damage to financial stability, that SIFIs themselves lack sufficient

incentives to take precautions against their own failures, that reliance

on extraordinary government interventions going forward would invite

moral hazard and lead to competitive distortions, and that the pre-crisis

regulatory focus on microprudential risks to individual financial

firms needed to be broadened to include threats to the overall stability

of the financial system.

In keeping with these lessons, post-crisis regulatory

reform has placed great weight on “macroprudential” regulation, which

seeks to address threats to financial stability. Section 165 of the

Dodd-Frank Act pursues this goal by empowering the Board to establish

enhanced regulatory standards for “large, interconnected financial

institutions” that “are more stringent than the standards . . . applicable

to [financial institutions] that do not present similar risks to the

financial stability of the United States” and “increase in stringency”

in proportion to the systemic importance of the financial institution

in question.2 Section 165(b)(1)(A)(i) of the act points

to risk-based capital requirements as a required type of enhanced

regulatory standard for SIFIs.

Rationales for a GSIB Surcharge

The Dodd-Frank

Act’s mandate that the Board adopt enhanced capital standards to mitigate

the risk posed to financial stability by certain large financial institutions

provides the principal statutory impetus for enhanced capital requirements

for SIFIs. Because the failure of a SIFI could undermine financial

stability and thus cause far greater negative externalities than could

the failure of a financial institution that is not systemically important,

a probability of default that would be acceptable for a non-systemic

firm may be unacceptably high for a SIFI. Reducing the probability

that a SIFI will default reduces the risk to financial stability.

The most straightforward means of lowering a financial firm’s probability

of default is to require it to hold a higher level of capital relative

to its risk-weighted assets than non-SIFIs are required to hold, thereby

enabling it to absorb greater losses without becoming insolvent.

There are also two secondary rationales for enhanced capital

standards for SIFIs. First, higher capital requirements create incentives

for SIFIs to shrink their systemic footprint, which further reduces

the risks these firms pose to financial stability. Second, higher

capital requirements may offset any funding advantage that SIFIs have

on account of being perceived as “too big to fail,” which reduces

the distortion in market competition caused by the perception and

the potential that counterparties may inappropriately shift more risk

to SIFIs, thereby increasing the risk those firms pose to the financial

system. Increased capital makes GSIBs more resilient in times of economic

stress, and, by increasing the capital cushion available to the firm,

may afford the firm and supervisors more time to address weaknesses

at the firm that could reverberate through the financial system were

the firm to fail.

The

Expected Impact Framework

By definition, a

GSIB’s failure would cause greater harm to financial stability than

the failure of a banking organization that is not a GSIB.3 Thus, if

all banking organizations are subject to the same risk-based capital

requirements and have similar probabilities of default, GSIBs will

impose far greater systemic risks than non-GSIBs will. The expected

impact framework addresses this discrepancy by subjecting GSIBs to

capital surcharges that are large enough that the expected systemic

loss from the failure of a given GSIB better approximates the expected

systemic loss from the failure of a BHC that is large but is not a

GSIB. (We will call this BHC the “reference BHC.”)

The expected loss from a given firm’s failure

can be computed as the systemic losses that would occur if that firm

failed, discounted by the probability of its failure. Using the acronyms

LGD (systemic loss given default), PD (probability of default), and

EL (expected loss), this idea can be expressed as follows: EL =

LGD * PD

The goal of a GSIB surcharge is to equalize the expected

loss from a GSIB’s failure to the expected loss from the failure of

a non-GSIB reference BHC: ELGSIB= ELr

By definition, a GSIB’s LGD is higher than that of a non-GSIB.

So to equalize EL between GSIBs and non-GSIBs, we must require each

GSIB to lower its PD, which we can do by requiring it to hold more

capital.

This implies that a GSIB must increase its capital level

to the extent necessary to reach a PD that is as many times lower

than the PD of the reference BHC as its LGD is higher than the LGD

of the reference BHC. (For example, suppose that a particular GSIB’s

failure would cause twice as much loss as the failure of the reference

BHC. In that case, to equalize EL between the two firms, we must require

the GSIB to hold enough additional capital that its PD is half that

of the reference BHC.) That determination requires the following components,

which we will consider in turn:

1. A method for creating “LGD scores” that

quantify the GSIBs’ LGDs

2. An LGD score for the reference BHC

3. A function relating a firm’s capital

ratio to its PD

Quantifying GSIB LGDs

The final rule employs two methods to measure GSIB

LGD:

Method 1 is based on the internationally accepted

GSIB surcharge framework, which produces a score derived from a firm’s

attributes in five categories: Size, interconnectedness, complexity,

cross-jurisdictional activity, and substitutability.

Method 2 replaces method 1’s substitutability category

with a measure of a firm’s reliance on short-term wholesale funding.

The preambles to the GSIB surcharge notice of proposed

rulemaking and final rule explain why these categories serve as proxies

for the systemic importance of a banking organization (and thus the

systemic harm that its failure would cause). They also explain how

the categories are weighted to produce scores under method 1 and method

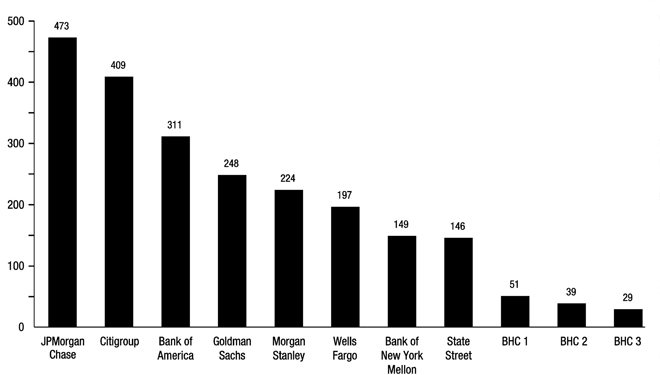

2. Table 1 conveys the Board’s estimates of the current scores for

the eight U.S. BHCs with the highest scores. These scores are estimated

from the most recent available data on firm-specific indicators of

systemic importance. The actual scores that will apply when the final

rule takes effect may be different and will depend on the future evolution

of the firm-specific indicator values.

Table 1—Top

eight scores under each method

Firm

Method 1 score

Method 2 score

JPMorgan Chase

473

857

Citigroup

409

714

Bank of America

311

559

Goldman Sachs

248

585

Morgan Stanley

224

545

Wells Fargo

197

352

Bank of New York

Mellon

149

213

State Street

146

275

This paper assumes that the relationships between the

scores produced by these methods and the firms’ systemic LGDs are

linear. In other words, it assumes that if firm A’s score is twice

as high as firm B’s score, then the systemic harms that would flow

from firm A’s failure would be twice as great as those that would

flow from firm B’s failure.

In fact, there is reason to believe that firm A’s failure

would do more than twice as much damage as firm B’s. (In other words,

there is reason to believe that the function relating the scores to

systemic LGD increases at an increasing rate and is therefore nonlinear.)

The reason is that at least some of the components of the two methods

appear to increase the systemic harms that would result from a default

at an increasing rate, while none appears to increase the resulting

systemic harm at a decreasing rate. For example, because the negative

priceimpact associated with the fire-sale liquidation of certain asset

portfolios increases with the size of the portfolio, systemic LGD

appears to grow at an increasing rate with the size, complexity, and

short-term wholesale funding metrics used in the methods. Thus, this

paper’s assumption of a linear relationship simplifies the analysis

while likely resulting in surcharges lower than those that would result

if the relationship between scores and systemic LGD were assumed to

be non-linear.

The Reference BHC’s Systemic LGD

Score

The reference BHC is a real or hypothetical

BHC whose LGD will be used in our calculations. The expected impact

framework requires that the reference BHC be a non-GSIB, but it leaves

room for discretion as to the reference BHC’s identity and LGD score.

Potential Approaches

The reference BHC score can be viewed as simply the LGD

score which, given the PD associated with the generally applicable

capital requirements, produces the highest EL that is consistent with

the purposes and mandate of the Dodd-Frank Act. The effect of setting

the reference BHC score to that LGD score would be to hold all GSIBs

to that EL level. The purpose of the Dodd-Frank Act is “to prevent

or mitigate risks to the financial stability of the United States

that could arise from the material financial distress or failure,

or ongoing activities, of large, interconnected financial institutions.”4 The following options appear to be conceptually

plausible ways of identifying the reference BHC for purposes of establishing

a capital requirement for GSIBs that lowers the expected loss from

the failure of a GSIB to the level associated with the failure of

a non-GSIB.

Option 1: A BHC with $50 billion in assets. Section

165(a)(1) of the Dodd-Frank Act calls for the Board to “establish

prudential standards for . . . bank holding companies with total consolidated

assets equal to or greater than $50,000,000,000 that (A) are more

stringent than the standards . . . applicable to . . . bank holding

companies that do not present similar risks to the financial stability

of the United States; and (B) increase in stringency.” Section 165

is the principal statutory basis for the GSIB surcharge, and its $50

billion figure provides a line below which it may be argued that Congress

did not believe that BHCs present sufficient “risks to the financial

stability of the United States” to warrant mandatory enhanced prudential

standards. It would therefore be reasonable to require GSIBs to hold

enough capital to reduce their expected systemic loss to an amount

equal to that of a $50 billion BHC that complies with the generally

applicable capital rules. Although $50 billion BHCs could have a range

of LGD scores based upon their other attributes, reasonable score

estimates for a BHC of that size are 3 under method 1 and 37 under

method 2.5

Option 2: A BHC with $250 billion in assets. The

Board’s implementation of the advanced approaches capital framework

imposes enhanced requirements on banking organizations with at least

$250 billion in consolidated assets. This level distinguishes the

largest and most internationally active U.S. banking organizations,

which are subject to other enhanced capital standards, including the

countercyclical capital buffer and the supplementary leverage ratio.6 The $250 billion threshold therefore provides another viable line

for distinguishing between the large, complex, internationally active

banking organizations that pose a substantial threat to financial

stability and those that do not pose such a substantial threat. Although

$250 billion BHCs could have a range of LGD scores based upon their

other attributes, reasonable score estimates for a BHC of that size

are 23 under method 1 and 60 under method 2.7

Option 3: The U.S. non-GSIB with the highest LGD score. Another plausible reference BHC is the actual U.S. non-GSIB BHC

that comes closest to being a GSIB—in other words, the U.S. non-GSIB

with the highest LGD score. Under method 1, the highest score for

a U.S. non-GSIB is 51 (the second-highest is 39). Under method 2,

the highest score for a U.S. non-GSIB is estimated to be 85 (the second-

and third-highest scores are both estimated to be 75).8

Option 4: A hypothetical BHC at the cutoff line between

GSIBs and non-GSIBs. Given that BHCs are divided into GSIBs and

non-GSIBs based on their systemic footprint and that LGD scores provide

our metric for quantifying firms’ systemic footprints, there must

be some LGD score under each method that marks the “cut-off line”

between GSIBs and non-GSIBs. The reference BHC’s score should be no

higher than this cut-off line, since the goal of the expected impact

framework is to lower each GSIB’s EL so that it equals the EL of a

non-GSIB. Under this option, the reference BHC’s score should also

be no lower than the cut-off line, since if it were lower,

then a non-GSIB firm could exist that had a higher LGD and therefore

(because it would not be subject to a GSIB surcharge) a higher

EL than GSIBs are permitted to have. Under this reasoning, the reference

BHC should have an LGD score that is exactly on the cut-off line between

GSIBs and non-GSIBs. That is, it should be just on the cusp of being

a GSIB.

What LGD score marks the cut-off line between GSIB and

non-GSIB? With respect to method 1, figure 1 shows that there is a

large drop-off between the eighth-highest score (146) and the ninth-highest

score (51). Drawing the cut-off line within this target range is reasonable

because firms with scores at or below 51 are much closer in size and

complexity to financial firms that have been resolved in an orderly

fashion than they are to the largest financial firms, which have scores

between three and nine times as high and are significantly larger

and more complex. We will choose a cut-off line at 130, which is at

the high end of the target range. This choice is appropriate because

it aligns with international standards and facilitates comparability

among jurisdictions. It also establishes minimum capital surcharges

that are consistent internationally.

Figure 1—Estimated

method 1 scores

Figure 1. Estimated method

1 scores

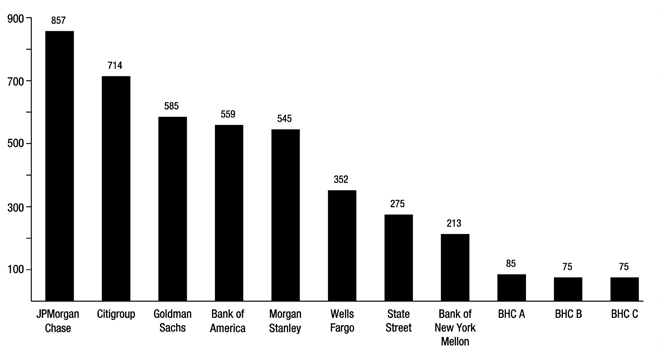

A similar approach can be used under method 2. Figure

2 depicts the estimated method 2 scores of the eleven U.S. BHCs with

the highest estimated scores. A large drop-off in the distribution

of scores with a significant difference in character of firms occurs

between firms with scores above 200 and firms with scores below 100.

The range between Bank of New York Mellon and the next-highest-scoring

firm is the most rational place to draw the line between GSIBs and

non-GSIBs: Bank of New York Mellon’s score is roughly 251 percent

of the score of the next highest-scoring firm, which is labeled BHC

A. (There is also a large gap between Morgan Stanley’s score and Wells

Fargo’s, but the former is only about 154 percent of the latter.)

This approach also generates the same list of eight U.S. GSIBs as

is produced by method 1. In selecting a specific line within this

range, we considered the statutory mandate to protect U.S. financial

stability, which argues for a method of calculating surcharges that

addresses the importance of mitigating the failure of U.S. GSIBs,

which are among the most systemic in the world. This would suggest

a cut-off line at the lower end of the target range. The lower threshold

is appropriate in light of the fact that method 2 uses a measure of

short-term wholesale funding in place of substitutability. Specifically,

short-term wholesale funding is believed to have particularly strong contagion

effects that could more easily lead to major systemic events, both

through the freezing of credit markets and through asset fire sales.

These systemic impacts support the choice of a threshold at the lower

end of the range for method 2.

Figure 2—Estimated

method 2 scores

Figure 2. Estimated method

2 scores

Although the failure of a firm with the systemic footprint

of BHC A poses a smaller risk to financial stability than does the

failure of one of the eight GSIBs, it is nonetheless possible that

the failure of a very large banking organization like BHC A, BHC B,

or BHC C could have a negative effect on financial stability, particularly

during a period of industry-wide stress such as occurred during the

2007-08 financial crisis. This provides additional support for our

decision to draw the line between GSIBs and non-GSIBs at 100 points,

at the lower end of the range between Bank of New York Mellon and

BHC A.

Note that we have set our method 2 reference BHC score

near the bottom of the target range and our method 1 reference BHC

score near the top of the target range. Due to the choice of reference

BHC in method 2, method 2 is likely to result in higher surcharges

than method 1. Calculating surcharges under method 1 in part recognizes

the international standards applied globally to GSIBs. Using a globally

consistent approach for establishing a baseline surcharge has benefits

for the stability of the entire financial system, which is globally

interconnected. At the same time, using an approach that results in

higher surcharges for most GSIBs is consistent with the statutory

mandate to protect financial stability in the United States and with

the risks presented by short-term wholesale funding.

Capital and Probability of Default

To implement

the expected impact approach, we also need a function that relates

capital ratio increases to reductions in probability of default. First,

we use historical data drawn from FR Y-9C regulatory reports from

the second quarter of 1987 through the fourth quarter of 2014 to plot

the probability distribution of returns on risk-weighted assets (RORWA)

for the 50 largest BHCs (determined as of each quarter), on a four-quarter

rolling basis.9 RORWA is defined as after-tax net income divided by risk-weighted

assets. Return on risk-weighted assets provides a better measure of

risk than return on total assets would, because the risk weightings

have been calibrated to ensure that two portfolios with the same risk-weighted

assets value contain roughly the same amount of risk, whereas two

portfolios with total assets of the same value can contain very different

amounts of risk depending on the asset classes in question.

We select this date range and set

of firms to provide a large sample size while focusing on data from

the relatively recent past and from very large firms, which are more

germane to our purposes. Data from the past three decades may be an

imperfect predictor of future trends, as there are factors that suggest

that default probabilities in the future may be either lower or higher

than would be predicted on the basis of the historical data.

On the one hand, these data do not

reflect many of the regulatory reforms implemented in the wake of

the 2007-08 financial crisis that are likely to reduce the probability

of very large losses and therefore the probability of default associated

with a given capital level. For example, the Basel 2.5 and Basel III

capital reforms are intended to increase the risk-sensitivity of the

risk weightings used to measure risk-weighted assets, which suggests

that the risk of losses associated with each dollar of risk-weighted

assets under Basel III will be lower than the historical, pre-Basel

III trend. Similarly, post-crisis liquidity initiatives (the liquidity

coverage ratio and the net stable funding ratio) should reduce the

default probabilities of large banking firms and the associated risk

of fire sales. Together, these reforms may lessen a GSIB’s probability

of default and potentially imply a lower GSIB surcharge.

On the other hand, however, extraordinary

government interventions during the time period of the dataset (particularly

in response to the 2007-08 financial crisis) undoubtedly prevented

or reduced large losses that many of the largest BHCs would otherwise

have suffered. Because one core purpose of post-crisis reform is to

avoid the need for such extraordinary interventions in the future,

the GSIB surcharge should be calibrated using data that include the

severe losses that would have materialized in the absence of such

intervention; because the interventions in fact occurred, using historical

RORWA data may lead us to underestimate the probability of default

associated with a given capital level. In short, there are reasons

to believe that the historical data underestimate the future trend,

and there are reasons to believe that those data overestimate the

future trend. Although the extent of the over- and underestimations

cannot be rigorously quantified, a reasonable assumption is that they

roughly cancel each other out.10

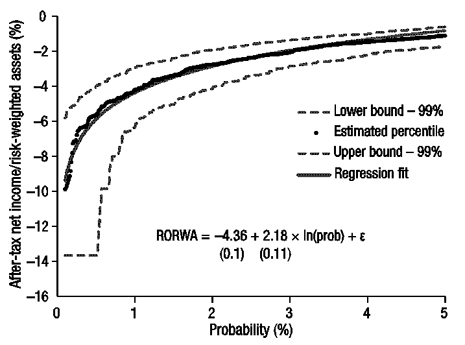

Figure 3 displays the estimated quantiles of ROWRA from

0.1 to 5.0. The sample quantiles are represented by black dots. The

dashed lines above and below the estimated quantiles represent a 99

percent confidence interval for each estimated quantile. As shown

in the figure, the uncertainty around more extreme quantiles is substantially

larger than that around less extreme quantiles. This is because actual

events relating to more extreme quantiles occur much less frequently

and are, as a result, subject to considerably more uncertainty. The

solid line that passes through the black dots is an estimated regression

function that relates the estimated value of the quantile to the natural

logarithm of the associated probability. The specification of the

regression function is provided in the figure which reports both the

estimated coefficients of the regression function and the standard

errors, in parentheses, associated with the estimated coefficients.

Figure 3—Returns on risk-weighted assets (RORWA)

(Bottom five percentiles, 50 largest BHCs in each quarter,

2Q87 through 4Q14)

Figure 3. Returns on risk-weighted

assets (RORWA)

Figure 3 shows that RORWA is negative (that is, the firm

experiences a loss) more than 5 percent of the time, with most losses

amounting to less than 4 percent of risk-weighted assets. The formula

for the logarithmic regression on this RORWA probability distribution

(with RORWA represented by y and the percentile associated with that

RORWA by x) is: y = 2.18 * ln(x) - 4.36

The inverse of this function, which

we will label p(RORWA), gives the probability that a particular

realization of RORWA,

Figure 4. DISPLAY EQUATION

$$

\tilde{R}

$$

will be less than or equal to a specified

level over a given year. That function is:

Next, assume that a BHC becomes non-viable and consequently

defaults if and only if its capital ratio k (measured in terms

of common equity tier 1 capital, or CET1) falls to some failure point f. (Note that k is a variable and f is a constant.)

We assume that RORWA and k are independent, which is appropriate

because the return on an asset should not depend to a significant

extent on the identity of the entity holding the asset or on that

entity’s capital ratio. We can now estimate the probability that a

BHC with capital level k will suffer sufficiently severe losses

(that is, a negative RORWA of sufficiently great magnitude) to bring

its capital ratio down to the failure point f. We are looking

for the probability that k will fall to f, that is,

the probability that k + RORWA = f. Solving for RORWA,

we get RORWA = f - k, which we can then plug into the

function above to find the probability of default as a function of

the capital ratio k:11

We

can now create a function that takes as its input a GSIB’s LGD score

and produces a capital surcharge for that GSIB. In the course of doing

so, we will find that the resulting surcharges are invariant to both

the failure point f and the generally applicable capital level that

the GSIB surcharge is held on top of, which means that we do not need

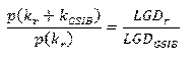

to make any assumption about the value of these two quantities. Recall

that the goal of the expected impact framework is to make the following

equation true:

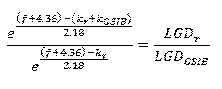

ELGSIB = ELr

Let kr be the generally applicable

capital level held by the reference BHC, and let kGSIB be the GSIB surcharge that a given GSIB is required

to hold on top of kr. Thus, the reference

BHC’s probability of default will be p(kr) and each GSIB’s probability of default will be p(kr + kGSIB), with

the value of kGSIB varying from firm to

firm. Because EL = LGD * PD, the equation above

can be expressed as:

As promised, the failure point f and

the baseline capital level kr prove to be

irrelevant. This is a consequence of the assumption that the quantiles

of the RORWA distribution are linearly related to the logarithm of

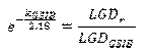

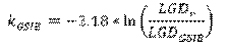

the quantile. Thus, we have:

The appropriate surcharge for a given GSIB

depends only on that GSIB’s LGD score and the chosen reference BHC’s

LGD score. Indeed, the surcharge does not even depend on the particular

values of those two scores, but only on the ratio between them. Thus,

doubling, halving, or otherwise multiplying both scores by the same

constant will not affect the resulting surcharges. And since each

of our reference BHC options was determined in relation to the LGD

scores of actual firms, any multiplication applied to the calculation

of the firms’ LGD scores will also carry over to the resulting reference

BHC scores.

Note that the specific GSIB surcharge depends on the slope

coefficient that determines how the quantiles of the RORWA distribution

change as the probability changes. The empirical analysis presented

in figure 3 suggests a value for the slope coefficient of roughly

2.18; however, there is uncertainty regarding the true population

value of this coefficient. There are two important sources of uncertainty.

First, the estimated value of 2.18 is a statistical estimate that

is subject to sampling uncertainty. This sampling uncertainty is characterized

in terms of the standard error of the coefficient estimate, which

is 0.11 (as reflected in parentheses beneath the point estimate in

figure 3). Under standard assumptions, the estimated value of the

slope coefficient is approximately normally distributed with a mean of

2.18 and a standard deviation of 0.11. A 99 percent confidence interval

for the slope coefficient ranges from approximately 1.9 to 2.4.

Second, there is additional uncertainty around the slope

coefficient that arises from uncertainty as to whether the data sample

used to construct the estimated slope coefficient is indicative of

the RORWA distribution that will obtain in the future. As discussed

above, there are reasons to believe that the future RORWA distribution

will differ to some extent from the historical distribution. Accordingly,

the 99 percent confidence interval for the slope coefficient that

is presented above is a lower bound to the true degree of uncertainty

that should be attached to the slope coefficient.

We can now use the GSIB surcharge formula and

99 percent confidence interval presented above to compute the ranges

of capital surcharges that would obtain for each of the reference

BHC options discussed above. Table 2 presents method 1 surcharge ranges

and table 3 presents method 2 surcharge ranges. The low estimate in

each cell was computed using the surcharge formula above with the

value of the slope coefficient at the low end of the 99 percent confidence

interval (1.9); the high end was computed using the value of the slope

coefficient at the high end of that interval (2.4).

Table 2—Method

1 surcharge ranges for each reference BHC (%)

Firm

Method 1 score

$50 billion reference BHC

$250 billion reference BHC

Non-GSIB with highest LGD

Reference BHC LGD = 130

JPMorgan Chase

473

9.6,

12.4

5.7,

7.4

4.2,

5.5

2.5,

3.2

Citigroup

409

9.3,

12.1

5.5,

7.1

4.0,

5.1

2.2,

2.8

Bank of America

311

8.8,

11.4

4.9,

6.4

3.4,

4.4

1.7,

2.1

Goldman Sachs

248

8.4,

10.9

4.5,

5.8

3.0,

3.9

1.2,

1.6

Morgan Stanley

224

8.2,

10.6

4.3,

5.6

2.8,

3.6

1.0,

1.3

Wells Fargo

197

8.0,

10.3

4.1,

5.3

2.6,

3.3

0.8,

1.0

Bank of New York

Mellon

149

7.4,

9.6

3.6,

4.6

2.0,

2.6

0.3,

0.3

State Street

146

7.4,

9.6

3.5,

4.5

2.0,

2.6

0.2,

0.3

Reference score

3

23

51

130

Table 3—Method

2 surcharge ranges for each reference BHC (%)

Firm

Method 2 score

$50 billion reference BHC

$250 billion reference BHC

Non-GSIB with highest LGD

Reference BHC LGD = 100

JPMorgan Chase

857

6.0,

7.7

5.1,

6.5

4.4,

5.7

4.1,

5.3

Citgroup

714

5.6,

7.3

4.7,

6.1

4.0,

5.2

3.7,

4.8

Goldman Sachs

585

5.2,

6.8

4.3,

5.6

3.7,

4.7

3.4,

4.3

Bank of America

559

5.2,

6.7

4.2,

5.5

3.6,

4.6

3.3,

4.2

Morgan Stanley

545

5.1,

6.6

4.2,

5.4

3.5,

4.6

3.2,

4.2

Wells Fargo

352

4.3,

5.5

3.4,

4.4

2.7,

3.5

2.4,

3.1

State Street

275

3.8,

4.9

2.9,

3.7

2.2,

2.9

1.9,

2.5

Bank of New York

Mellon

213

3.3,

4.3

2.4,

3.1

1.7,

2.3

1.4,

1.9

Reference score

37

60

85

100

Surcharge Bands

The analysis above suggests a range of capital surcharges

for a given LGD score. To obtain a simple and easy-to-implement surcharge

rule, we will assign surcharges to discrete “bands” of scores so that

the surcharge for a given score falls in the lower end of the range

suggested by the results shown in tables 2 and 3. The bands will be

chosen so that the surcharges for each band rise in increments of

one half of a percentage point. This sizing will ensure that modest

changes in a firm’s systemic indicators will generally not cause a

change in its surcharge, while at the same time maintaining a reasonable

level of sensitivity to changes in a firm’s systemic footprint. Because

small changes in a firm’s score will generally not cause a change

to the firm’s surcharge, using surcharge bands will facilitate capital

planning by firms subject to the rule.

We will omit the surcharge band associated with a 0.5

percent surcharge. This tailoring for the least-systemic band of scores

above the reference BHC score is rational in light of the fixed costs

of imposing a firm-specific capital surcharge; these costs are likely

not worth incurring where only a small surcharge would be imposed.

(The internationally accepted GSIB surcharge framework similarly lacks

a 0.5 percent surcharge band.) Moreover, aminimum surcharge of 1.0

percent for all GSIBs accounts for the inability to know precisely

where the cut-off line between a GSIB and a non-GSIB will be at the

time when a failure occurs, and the surcharge’s purpose of enhancing

the resilience of all GSIBs.

We will use 100-point fixed-width bands, with a 1.0 percent

surcharge band at 130-229 points, a 1.5 percent surcharge band at 230-329 points, and so on. These surcharge bands fall in the lower

end of the range suggested by the results shown in tables 1 and 2.

The analysis above suggests that the surcharge should

depend on the logarithm of the LGD score. The logarithmic function

could justify bands that are smaller for lower LGD scores and larger

for higher LGD scores. For the following reasons, however, fixed-width

bands are more appropriate than expanding-width bands.

First, fixed-width surcharge bands

facilitate capital planning for less-systemic firms, which would otherwise

be subject to a larger number of narrower bands. Such small bands

could result in frequent and in some cases unforeseen changes in those

firms’ surcharges, which could unnecessarily complicate capital planning

and is contrary to the objective of ensuring that relatively small

changes in a firm’s score generally will not alter the firm’s surcharge.

Second, fixed-width surcharge bands are appropriate in

light of several concerns about the RORWA dataset and the relationship

between systemic indicators and systemic footprint that are particularly

relevant to the most systemically important financial institutions.

Larger surcharge bands for the most systemically important firms would

allow these firms to expand their systemic footprint materially within

the band without augmenting their capital buffers. That state of affairs

would be particularly troubling in light of limitations on the data

used in the statistical analysis above.

In particular, while the historical RORWA dataset used

to derive the function relating a firm’s LGD score to its surcharge

contains many observations for relatively small losses, it contains

far fewer observations of large losses of the magnitude necessary

to cause the failure of a firm that has a very large systemic footprint

and is therefore already subject to a surcharge of (for example) 4.0

percent. This paucity of observations means that our estimation of

the probability of such losses is substantially more uncertain than

is the case with smaller losses. This is reflected in the magnitude

of the standard error range associated with our regression analysis,

which is large and rapidly expanding for high LGD scores. Given this

uncertainty, as well as the Board’s Dodd-Frank Act mandate to impose

prudential standards that mitigate risks to financial stability, we

should impose a higher threshold of certainty on the sufficiency of

capital requirements for the most systemically important financial

institutions.

Two further shortcomings of the RORWA dataset make the

case for rejecting ever-expanding bands even stronger. First, the

frequency of extremely large losses would likely have been higher in

the absence of extraordinary government actions taken to protect financial

stability, especially during the 2007-08 financial crisis. As discussed

above, the GSIB surcharge should be set on the assumption that extraordinary

interventions will not recur in the future (in order to ensure that

they will not be necessary in the future), which means that firms

need to hold more capital to absorb losses in the tail of the distribution

than the historical data would suggest. Second, the historical data

are subject to survivorship bias, in that a given BHC is only included

in the sample until it fails (or is acquired). If a firm fails in

a given quarter, then its experience in that quarter is not included

in the dataset, and any losses realized during that quarter (including

losses realized only upon failure) are therefore left out of the dataset,

leading to an underestimate of the probability of such large losses.

Additionally, as discussed above, our assumption of a

linear relationship between a firm’s LGD score and the risk that its

failure would pose to financial stability likely understates the surcharge

that would be appropriate for the most systemically important firms.

As noted above, there is reason to believe that the damage to the

economy increases more rapidly as a firm grows in size, complexity,

reliance on short-term wholesale funding, and perhaps other GSIB metrics.

Finally, fixed-width bands are preferable to expanding-width

bands because they are simpler and therefore more transparent to regulated

entities and to the public.

Alternatives to the Expected Impact Framework

Federal Reserve staff considered various alternatives to the expected

impact framework for calibrating a GSIB surcharge. All available methodologies

are highly sensitive to a range of assumptions.

Economy-Wide Cost-Benefit Analysis

One

alternative to the expected impact framework is to assess all social

costs and benefits of capital surcharges for GSIBs and then set each

firm’s requirement at the point where marginal social costs equal

marginal social benefits. The principal social benefit of a GSIB surcharge

is a reduction in the likelihood and severity of financial crises

and crisis-induced recessions. Assuming that capital is a relatively

expensive source of funding, the potential costs of higher GSIB capital

requirements come from reduced credit intermediation by GSIBs (though

this would be offset to some extent by increased intermediation by

smaller banking organizations and other entities), a potential loss

of any GSIB scale efficiencies, and a potential shift of credit intermediation

to the less-regulated shadow banking sector. The GSIB surcharges that

would result from this analysis would be sensitive to assumptions

about each of these factors.

One study produced by the Basel Committee on Banking Supervision

(with contributions from Federal Reserve staff) finds that net social

benefits would be maximized if generally applicable common equity

requirements were set to 13 percent of risk-weighted assets, which

could imply that a GSIB surcharge of up to 6 percent would be socially

beneficial.12 The surcharges produced by the expected

impact framework are generally consistent with that range.

That said, cost-benefit analysis

was not chosen as the primary calibration framework for the GSIB surcharge

for two reasons. First, it is not directly related to the mandate

provided by the Dodd-Frank Act, which instructs the Board to mitigate

risks to the financial stability of the United States. Second, using

cost-benefit analysis to directly calibrate firm-specific surcharges

would require more precision in estimating the factors discussed above

in the context of surcharges for individual firms than is now attainable.

Offsetting the Too-Big-To-Fail

Subsidy

It is generally agreed that GSIBs enjoyed

a “too-big-to-fail” funding advantage prior to the crisis

and ensuing regulation, and some studies find that such a funding

advantage persists. Any such advantage derives from the belief of

some creditors that the government might act to prevent a GSIB from

defaulting on its debts. This belief leads creditors to assign a lower

credit risk to GSIBs than would be appropriate in the absence of this

government “subsidy,” with the result that GSIBs can borrow at lower

rates. This creates an incentive for GSIBs to take on even more leverage

and make themselves even more systemic (in order to increase the value

of the subsidy), and it gives GSIBs an unfair advantage over less

systemic competitors.

In theory, a GSIB surcharge could be calibrated to offset

the too-big-to-fail subsidy and thereby cancel out these undesirable

effects. The surcharge could do so in two ways. First, as with an

insurance policy, the value of a potential government intervention

is proportional to the probability that the intervention will actually

occur. A larger buffer of capital lowers a GSIB’s probability of default

and thereby makes potential government intervention less likely. Put

differently, a too-big-to-fail subsidy leads creditors to lower the

credit risk premium they charge to GSIBs; by lowering credit risk,

increased capital levels would lower the value of any discount in

the credit risk premium. Second, banking organizations view capital

as a relatively costly source of funding. If it is, then a firm with

elevated capital requirements also has a concomitantly higher cost

of funding than a firm with just the generally applicable capital

requirements. And this increased cost of funding could, if calibrated

correctly, offset any cost-of-funding advantage derived from the too-big-to-fail

subsidy.

A surcharge calibration intended to offset any too-big-to-fail

subsidy would be highly sensitive to assumptions about the size of

the subsidy and about the respective costs of equity and debt as funding

sources at various capital levels. These quantities cannot currently

be estimated with sufficient precision to arrive at capital surcharges

for individual firms. Thus, the expected impact approach is preferable

as a primary framework for setting GSIB surcharges.

Cf. Dodd-Frank Act section 165(a)(1), which instructs the Board to

apply more stringent prudential standards to certain large financial

firms “[i]n order to prevent or mitigate risks to the financial stability

of the United States that could arise from the material financial

distress or failure . . . of large, interconnected financial institutions.”

As illustrated by the financial crisis that led Congress to enact

the Dodd-Frank Act, financial instability can lead to a wide range

of social harms, including the declines in employment and GDP growth

that are associated with an economic recession.

These estimates were produced by plotting the estimated scores of

six U.S. BHCs with total assets between $50 billion and $100 billion

against their total assets, running a linear regression, and finding

the score implied by the regression for a $50 billion firm. These

firms’ scores were estimated using data from the sources described

in the general note to table 1, except that figures for the short-term

wholesale funding component of method 2 were estimated using FR Y-9C

data from the first quarter of 2015 and Federal Reserve quantitative

impact study (QIS) data as of the fourth quarter of 2014. Scores for

firms with total assets below $50 billion were not estimated (and

therefore were not included in the regression analysis) because the

Federal Reserve does not collect as much data from those firms.

These estimates were produced by applying the approach described

in footnote 5 to 10 U.S BHCs with total assets between $100 billion

and $400 billion. Bank of New York Mellon and State Street, which

have total assets within that range, were excluded from the sample

because they are GSIBs and the expected impact framework assumes that

the reference BHC is a non-GSIB.

These estimates were produced using data from the sources described

in the general note to table 1, except that figures for the short-term

wholesale funding component of method 2 were estimated using FR Y-9C

data from the first quarter of 2015 and Federal Reserve quantitative

impact study (QIS) data as of the fourth quarter of 2014.

Because Basel I risk-weighted assets data are only available from

1996 onward, risk-weighted assets data for earlier years are estimated

by back-fitting the post-1996 ratio between risk-weighted assets and

total assets onto pre-1996 total assets data. See Andrew Kuritzkes

and Til Schuermann (2008), “What We Know, Don’t Know, and Can’t Know

about Bank Risk: A View from the Trenches,” University of Pennsylvania,

Financial Institutions Center paper #06-05, http://fic.wharton.upenn.edu/fic/papers/06/0605.pdf.

The concept of risk aversion provides additional support for this

assumption. While the failure of a GSIB in any given year is unlikely,

the costs from such a failure to financial stability could be severe.

By contrast, any costs from higher capital surcharges will be distributed

more evenly among different states of the world. Presumably society

is risk-averse and, in a close case, would prefer the latter set of

costs to the former. While this paper does not attempt to incorporate

risk aversion into its quantitative analysis, that concept does provide

additional support for the decision not to discount the historical

probability of large losses in light of post-crisis regulatory reforms.

This paper treats dollars of risk-weighted assets as equivalent regardless

of whether they are measured under the risk weightings of Basel I

or of Basel III. This treatment makes sense because the two systems

produce roughly comparable results and there does not appear to be

any objectively correct conversion factor for converting between them.

See Basel Committee on Banking Supervision (2010), An Assessment

of the Long-Term Economic Impact of Stronger Capital and Liquidity

Requirements (Basel, Switzerland: Bank for International Settlements,

August), p. 29, www.bis.org/publ/bcbs173.pdf. The study finds that

a capital ratio of 13 percent maximizes net benefits on the assumption

that a financial crisis can be expected to have moderate permanent

effects on the economy.