Community banks engage with third parties

to compete in and respond to an evolving financial services landscape.

Third-party relationships can offer community banks access to new

technologies, risk-management tools, human capital, delivery channels,

products, services, and markets. A community bank’s reliance

on third parties, however, reduces its direct operational control

over activities1 and may introduce new risks or increase existing risks, including,

but not limited to, operational, compliance, financial, and strategic

risks.

Due to the varied risks associated with

third-party relationships, it is important for community banks to

appropriately identify, assess, monitor, and control these risks as

well as ensure that activities are performed in a safe and sound manner

and in compliance with applicable laws and regulations.2 These laws and regulations include, but are not limited to, those

designed to protect consumers (such as fair lending laws and prohibitions

against unfair, deceptive, or abusive acts or practices) and those

addressing financial crimes (such as fraud and money laundering).

Engaging a third party does not diminish or remove

a bank’s responsibility to operate in a safe and sound manner

and to comply with applicable legal and regulatory requirements, including

consumer protection laws and regulations, just as if the bank were

to perform the service or activity itself. A community bank may

engage an external party to conduct aspects of its third-party risk

management. However, the bank cannot abrogate its responsibility to

employ effective risk-management practices, including when using a

third party to conduct third-party risk management on behalf of the

bank.

About This

Guide

In June 2023, the Board of Governors

of the Federal Reserve System (Board), the Federal Deposit Insurance

Corporation (FDIC), and the Office of the Comptroller of the Currency

(OCC) (collectively, the agencies) issued the Interagency Guidance

on Third-Party Relationships: Risk Management (TPRM Guidance).3 The TPRM Guidance includes

sound risk-management principles for banking organizations to consider

when developing and implementing risk-management practices for all

stages in the life cycle of third-party relationships.

This guide is intended to assist community banks when developing

and implementing their third-party risk-management practices. This

guide is not a substitute for the TPRM Guidance.4 Rather, it is intended to be a resource

for community banks to consider when managing the risk of third-party

relationships. This guide is not a checklist and does not prescribe

specific risk-management practices or establish any safe harbors for

compliance with laws or regulations. While this guide is intended

for use by community banks, other banks may find it useful. Some additional

resources that can help support a bank’s development and implementation

of its risk-management program are listed in the appendix to this

guide. The agencies underscore that supervisory guidance does not

have the force and effect of law and does not impose any new requirements

on banks.

Guide Contents

The guide provides potential considerations, resources,

and examples through each stage of the third-party risk-management

life cycle and is organized under the following topics:

Governance. Considerations for governance related to third-party risk.

Appendix. Additional resources that can help support a bank’s development

and implementation of its third-party risk-management practices.

Excerpts from the TPRM Guidance are also highlighted

within boxes in each section.

TPRM Guidance

A banking

organization can be exposed to adverse impacts, including substantial

financial loss and operational disruption, if it fails to appropriately

manage the risks associated with third-party relationships. Therefore,

it is important for a banking organization to identify, assess, monitor,

and control risks related to third-party relationships.

Risk Management

Not all third-party relationships present

the same level of risk, and therefore not all relationships require

the same level of oversight. As part of sound risk management, community

banks apply more rigorous risk-management practices throughout the

third-party relationship life cycle for third parties that support

higher-risk activities, including critical activities. A community

bank may adjust and update its third-party risk-management practices

commensurate with its size, complexity, and risk profile by periodically

analyzing the risks associated with each third-party relationship.

It is important to involve bank staff with the requisite knowledge

and skills in each stage of the risk-management life cycle.

This guide includes considerations illustrating how a

community bank may apply risk-management practices in different stages

of the third-party relationship life cycle. An important initial step

is identifying third-party relationships that support higher-risk

activities, including critical activities. In determining whether

an activity is higher risk, banks may assess various factors, such

as if the third party has access to sensitive data (including customer

data), processes transactions, or provides essential technology and

business services.

TPRM Guidance

As

part of sound risk management, banking organizations engage in more

comprehensive and rigorous oversight and management of third-party

relationships that support higher-risk activities, including critical

activities. Characteristics of critical activities may include those

activities that could:

cause a banking organization to face

significant risk if the third party fails to meet expectations;

have significant customer impacts;

or

have a significant impact on a banking

organization’s financial condition or operations.

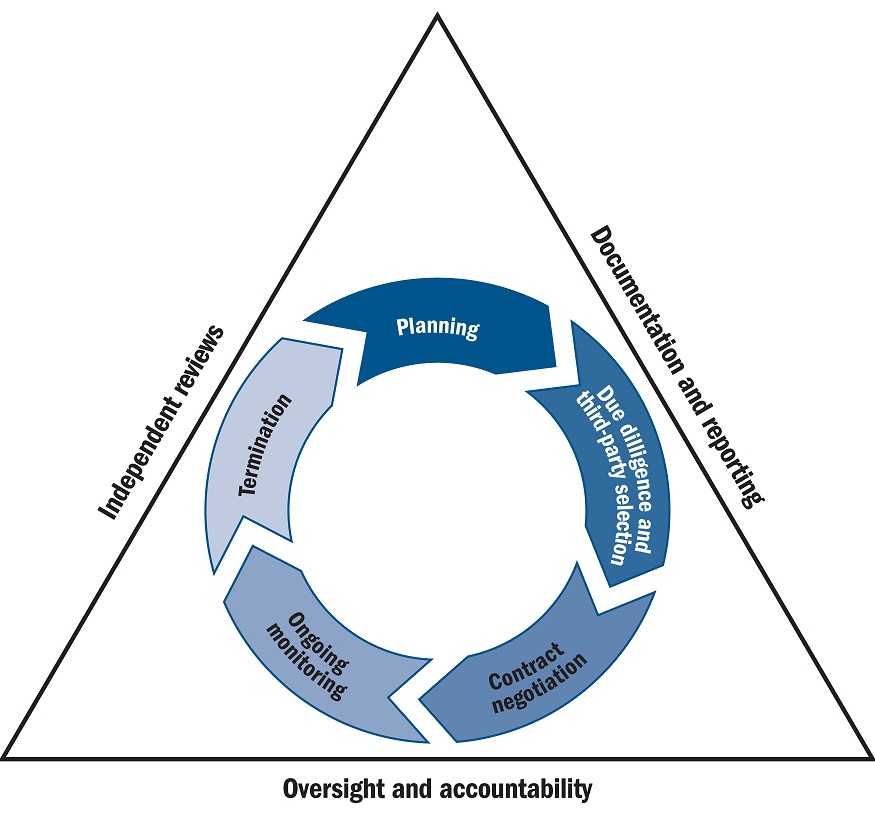

Third-Party

Relationship Life Cycle

Effective third-party

risk management generally follows a continuous life cycle for third-party

relationships. The five stages of the life cycle are set forth in

figure 1, surrounded by the governance practices of Oversight and

Accountability, Independent Reviews, and Documentation and Reporting.

For every stage, a community bank’s level

or type of oversight may vary, commensurate with its size, complexity,

and risk profile as well as with the nature of the specific third-party

relationship.

Figure 1. Stages of the risk-management

life cycle

Planning

Careful planning enables a community bank to consider

potential risks in the proposed third-party relationship. In addition,

risk assessments are an important component of managing third-party

relationships and help a bank evaluate the extent of risk-management

resources and practices for effective oversight of the proposed third-party

relationship throughout the subsequent stages of the third-party relationship

life cycle.

TPRM Guidance

As

part of sound risk management, effective planning allows a banking

organization to evaluate and consider how to manage risks before entering

into a third-party relationship.

Potential Considerations

What are the underlying activities

to be performed, and what are the bank and third party’s prospective

roles in the activities?

What legal and compliance requirements

will apply to the prospective third-party activities?

What are the benefits of the relationship,

and how would the relationship align with the bank’s strategic

plan?

What risk-management and governance

practices (including internal controls) will be necessary to manage

and mitigate the potential risks?

What are the financial implications

of entering into and maintaining the business arrangement?

What are the direct contractual costs

and indirect costs to augment or alter bank staffing, processes, and

technology?

Do the expected benefits of the relationship

exceed the potential costs and risks?

How will the bank integrate third-party

technology with the bank’s existing systems and infrastructure?

What changes would need to be made to the bank’s technology

to ensure compatibility, and what would be the associated risks and

costs? Does staff have the requisite skills to manage risks associated

with integrating the third party’s technology into the bank’s

environment (if not, how will the bank integrate the technology)?

What physical and/or system access

would the third party have to bank facilities, systems, and records,

and what recordkeeping processes would the bank require the third

party to implement?

What interaction will the third party

have with customers, and how would customer complaints be handled?

What are the information security

implications, and how will the third party access, process, and protect

customers’ information?

Has the bank considered how to exit

the activity or transition the activity to an alternative third party

or in-house?

Potential Sources

of Information

The bank’s strategic plan to

assess the proposed activity’s alignment with the bank’s

risk appetite, policies, and business objectives.

The bank’s budget or cost-benefit

analysis to assess the financial considerations of the relationship.

The bank’s human resources staff

to assess whether management and staff have the expertise and capacity

to manage the relationship.

The bank’s internal policies,

processes, and controls to assess the impact to the bank of entering

into and managing the proposed relationship.

The bank’s inventory of existing

third-party relationships to assess whether an existing relationship

could support the new activity.

The bank’s technology infrastructure

and staff to assess how readily it could integrate with a third party

to support the new activity.

The perspectives of the bank’s

subject matter experts, including those in information technology,

legal, and compliance risk.

Board policies, including risk limits,

to assess alignment with the proposed third-party relationship.

Example: Planning

A community bank experiences financial losses due to a

recent surge in fraudulent transactions. The bank’s management

identifies the root cause and decides to introduce additional internal

controls and training to mitigate future losses. Management contemplates

two alternatives for carrying out new preventative measures.

The first approach is to allocate internal resources to

develop and implement new internal controls and training across the

bank. The second approach is to outsource to a third party, which

will develop new fraud controls and applicable employee training.

When evaluating the in-house option, the bank’s

management

assesses its existing in-house expertise

and capabilities, including the ability to ensure that new fraud controls

would comply with applicable laws and regulations;

evaluates whether dedicating internal

resources to this project will strain the bank’s business-as-usual

operations; and

assesses the timeline for completing

the project internally and whether it aligns with the urgency to strengthen

the bank’s defenses against fraud incidents.

When evaluating whether to outsource this project,

the bank’s management

considers data security risk in light

of the fact that the third party would have access to confidential

bank and customer information during the project;

considers the potential compliance

risk exposure from a third party, such as the risk that new internal

controls would not ensure compliance with applicable laws and regulations;

assesses the financial feasibility

of the outsourcing option by comparing estimated direct and indirect

costs with the bank’s budget;

determines minimum requirements for

the service level agreement, which will establish clear performance

standards for the third party, supported by a resolution mechanism;

and

evaluates whether the bank has appropriate

policies and internal controls as well as sufficient resources, to

adequately monitor the third party’s performance.

The examples are provided for illustrative

purposes, are not comprehensive, and will not be applicable to all

situations.

Due Diligence and Third-Party Selection

Due diligence is the process by which a community

bank assesses, before entering into a third-party relationship, a

particular third party’s ability to perform the activity as

expected, adhere to the community bank’s policies, comply with

all applicable laws and regulations, and conduct the activity in a

safe and sound manner. Effective due diligence assists with the selection

of capable and reliable third parties to perform activities for, through,

or on behalf of the community bank. If the bank cannot obtain desired

due diligence information from the third party, the bank may consider

alternative information, controls, or monitoring.

TPRM Guidance

Conducting

due diligence on third parties before selecting and entering into

third-party relationships is an important part of sound risk management.

It provides management with the information needed about potential

third parties to determine if a relationship would help achieve a

banking organization’s strategic and financial goals. The due

diligence process also provides the banking organization with the

information needed to evaluate whether it can appropriately identify,

monitor, and control risks associated with the particular third-party

relationship.

Potential Considerations

Has the third party demonstrated

financial and operational capability to meet its obligations to the

bank? If no, what alternative information is available?

What resources and expertise are

available at the third party to support the activity?

What third-party policies, processes,

and internal controls support performance of the service in alignment

with the bank’s expectations and standards?

Has the third party demonstrated an

ability to comply with applicable laws and regulations, including

anti-money laundering and countering the financing of terrorism (AML/CFT)

as well as fair lending and consumer protection laws and regulations

(as applicable)?

Is the third party’s information

security program consistent with the bank’s program and expectations

related to protecting the confidentiality, integrity, and availability

of information?

Does the third party demonstrate

the ability to effectively operate through and recover from both internal

and external operational incidents or disruptions?

How has the third party performed

in the past during periods of economic or financial stress?

Does the third party rely on subcontractors,

and could that reliance pose additional or heightened risk to the

bank?

Does the third party use technologies

that could introduce additional risk?

Does the third party have a robust

consumer complaint program? Does it have a history of prompt and satisfactory

resolution of consumer complaints?

Is the third party involved in ongoing

litigation or other public matters of concern?

Can the third party demonstrate that

it has successfully provided the prospective services for other banks

or similar clients?

Potential Sources

of Information

The third party’s audited financial

statements and other financial information to assess the third party’s

financial condition.

The third party’s licenses and

any other legal authority necessary to perform the activity.

The third party’s relevant policies

and procedures, including those related to AML/CFT, to assess the

effectiveness of its risk-management practices, control environment,

and alignment with the bank’s expectations and standards and

with applicable legal requirements.

Independent reviews of the effectiveness

of those policies and procedures, including AML/CFT.

The third party’s strategic

plan or other disclosures to assess whether the business strategy

and its agreements with other entities pose new or increased risks.

The third party’s staffing

levels and qualifications to assess whether the third party’s

resources can fulfill its obligations to the bank, including those

of principals and other key personnel related to the activity.

The third party’s training

program to assess if its employees understand their duties and responsibilities,

are knowledgeable about applicable laws and regulations, and have

requisite certifications and licenses.

The volume and nature of consumer

complaints against the third party.

The Office of Foreign Assets Control

Specially Designated Nationals and Blocked Persons list (“SDN

List”) and all other sanctions lists to ensure the third party

and its employees, contractors, or grantees are not sanctioned by

the U.S. government.

System and Organization Controls (SOC)

reports, independent assessments, and industry certifications to assess

the third party’s operational risk management and internal controls.

Audit reports to assess the third

party’s risk management and internal controls.

References and feedback from peer

institutions or clients that are currently using the third party’s

service.

The third party’s current insurance

coverage to determine if sufficient for the activity.

Disclosures and information in the

media or in any of the third party’s publications, including

its website, to assess potential risks to the bank.

Internet searches of the third party’s

company name to determine whether it has been partnered with institutions

subject to consent orders related to third-party transactions or conducts

business with companies that misrepresent deposit insurance coverage.

Example: Due Diligence

A community bank is exploring enhancements to its

information security program with respect to its user access practices.

The bank’s board and management explore strengthening its user

access practices by implementing multi-factor authentication for user

access to the bank’s network by contracting for an authentication

service offered by its core service provider. Although the bank has

an established relationship with its core service provider, the new

service is outside the scope of the current contracted services. Bank

management requests that the core service provider submit a proposal,

including scope and pricing, for the new service.

The bank completes a third-party risk assessment and identifies potential

risk issues, including, but not limited to, risk associated with the

service provider’s technical expertise and training, robustness

of controls, and system connectivity. The results of this risk assessment

help guide the bank’s due diligence. As part of its due diligence

process, the bank evaluates a range of information regarding the financial,

compliance, and operational aspects of the prospective expanded relationship.

The bank’s management takes the following measures

to conduct due diligence and evaluate the core service provider’s

capabilities, expertise, and resources related to the new service:

Reviews the core service provider

proposal to understand the financial cost, time, and resources required

for implementation of the authentication service. This review leverages

bank staff’s existing knowledge and experience with the core

service provider’s technologies and services;

Reviews the core service provider’s

staffing levels and qualifications to evaluate whether the core service

provider has sufficient skill and technical expertise to implement

the new service;

Reviews the core service provider’s

proposed contract to evaluate key terms, costs, timeline, and other

service terms;

Evaluates the core service provider’s

proposed implementation plan to assess its impact on bank operations,

including any proposed downtime, and its ability to adhere to the

expected timeline; and

Compares the core service provider’s

proposal with the bank’s existing policies for security. Specifically,

the bank reviews the core service provider’s security policies

regarding customers’ data and authentication of users and devices.

The examples are provided for illustrative

purposes, are not comprehensive, and will not be applicable to all

situations.

Contract Negotiation

Before entering a contractual relationship with a third party, a

community bank typically considers contract provisions that meet its

business objectives, regulatory obligations, and risk-management policies

and procedures. The community bank typically negotiates contract provisions

that facilitate effective risk management and oversight, including

terms that specify the expectations and obligations of both the community

bank and the third party. When a community bank has limited negotiating

power, it is important for bank management to understand any resulting

limitations and consequent risks. Possible actions that bank management

might take in such circumstances include determining whether the contract

can still meet the community bank’s needs, whether the contract

would result in increased risk to the community bank, and whether

residual risks are acceptable.

TPRM Guidance

. .

. a banking organization typically negotiates contract provisions

that will facilitate effective risk management and oversight and that

specify the expectations and obligations of both the banking organization

and the third party. . . . In difficult contract negotiations, including

when a banking organization has limited negotiating power, it is important

for the banking organization to understand any resulting limitations

and consequent risks.

Potential Considerations

To what extent does the contract specify

the parties’ responsibilities and cover all aspects of the relationship

(including costs, reimbursements, and other liabilities)?

What provisions does the bank need

to include regarding termination events (for example, default or force

majeure), continuity planning, and associated costs and fees?

What are the governance and escalation

protocols regarding the third party’s performance and security

measures or benchmarks?

To what extent does the contract

enable the bank to obtain timely information it needs to perform adequate

ongoing monitoring, demonstrate compliance with applicable laws and

regulations, and respond to regulatory requests? For example, will

the bank have access to application and loan data, account opening

and customer information, audit reports, suspicious activity monitoring

information, and reports to identify safety and soundness and consumer

compliance issues?

What arrangements will be negotiated

for sharing and using information, technology, and intellectual property?

Does the contract specify limitations

on the third party’s use and retention of data (including customer

data) related to the activity, including its disclosure, storage,

delivery to the bank, and destruction?

Does the contract appropriately address

the bank’s right to access its data at the third party and the

process by which the bank will access its records and data (including

customer data)?

When and how will the third party

notify the bank of a disruption, including degradation or interruptions

in delivery, and how will the third party assist the bank with continuation

of the activity?

When and how will the third party

notify the bank of strategic changes, such as mergers and acquisitions

and leadership changes?

What continuity plans, processes,

and controls will the third party maintain to ensure contract adherence,

including recovery time and recovery point objectives?

For higher-risk activities, including

critical activities, what are likely scenarios for breach of contract,

and has the bank considered the potential exposure and cost?

Potential Sources

of Information

The bank’s risk assessment and

due diligence findings to determine the provisions to include in the

contract.

The third party’s proposed service

level agreements to set applicable performance and security metrics.

Assessments from business units regarding

their business needs and customer service objectives to determine

performance and security measures to include in the contract.

Contract provisions outlining the bank’s

access to the third party’s audit, testing, and self-assessment

reports for ongoing monitoring.

Legal, compliance, and other stakeholders’

perspectives to advise bank management on the contract provisions

to appropriately protect the bank’s interests.

Example: Contract Negotiation

A community bank seeks to upgrade its computing capabilities

to meet competitive challenges and customer demands. The bank’s

management identifies several benefits in outsourcing its computing

for higher-risk activities, including critical activities, and determines

that contracting with a service provider is the appropriate option

for its business needs.

When reviewing the contract

with the bank’s subject matter experts and its legal counsel,

the bank’s management identifies that the provider’s contract

contains standard provisions related to audit rights and determines

them to be inadequate for ongoing monitoring. The bank’s board

and management want the contractual right to review the service provider’s

reports of its business continuity and disaster recovery tests performed

on a monthly basis or to periodically conduct on-site visits for certain

audit purposes. As a result, bank management finds that the standard

contractual provisions would present challenges to the bank in complying

with its regulatory requirements, business objectives, and risk-management

needs.

To address these challenges with the service

provider, the bank’s management

requests that the service provider

modify the contract terms to require providing monthly test reports

to the bank and to allow the bank to conduct visits (either virtual

or on site);

considers if these modifications would

make the contract satisfactory for the bank’s regulatory requirements,

business objectives, and risk-management needs; and

conducts additional research on alternative

providers to determine if they will include contract terms that support

the bank’s regulatory requirements, business objectives, and

risk-management needs.

The examples are provided for illustrative

purposes, are not comprehensive, and will not be applicable to all

situations.

Ongoing Monitoring

A community bank’s ongoing monitoring of the third party’s

performance enables bank management to determine if the third party

is performing as required for the duration of the contract. The bank

may also use information from ongoing monitoring to adapt and refine

its risk-management practices.

TPRM Guidance

Ongoing

monitoring enables a banking organization to (1) confirm the quality

and sustainability of a third party’s controls and ability to

meet contractual obligations; (2) escalate significant issues or concerns,

such as material or repeat audit findings, deterioration in financial

condition, security breaches, data loss, service interruptions, compliance

lapses, or other indicators of increased risk; and (3) respond to

such significant issues or concerns when identified. . . . To gain

efficiencies or leverage specialized expertise, banking organizations

may engage external resources, refer to conformity assessments or

certifications, or collaborate when performing ongoing monitoring.

Potential

Considerations

Is the third party performing its

obligations under the contract?

Has the third party’s financial

condition changed, including declining revenues or increasing debt

obligations?

Has the third party complied with

applicable laws, regulations, and service level agreements?

Do audit and test results indicate

the third party is managing risks and meeting contractual obligations

and regulatory requirements effectively?

Is the third party demonstrating an

ability to maintain its systems within the bank’s availability

requirements (e.g., latency, bandwidth, and uptime)?

Is the third party demonstrating reliability

throughout its relationship with the bank?

How do the third party’s business

continuity and disaster recovery plans and practices demonstrate its

capability to respond and recover from service disruptions?

Has the third party maintained the

confidentiality, availability, and integrity of customer data (where

applicable) and the bank’s systems, information, and data?

Do reports from the third party align

with the bank’s internal reports and observations?

Has the third party’s performance

changed due to mergers, acquisitions, or divestitures?

Has the bank’s reliance on the

third party to conduct bank activities changed over the life of the

relationship?

For third parties that interact with

customers or access customer data, has the third party responded appropriately

to the bank’s requests for its records and information?

Have there been changes in the third

party’s strategy, corporate culture, leadership, or risk exposure?

If so, what is the impact on the relationship with the bank?

Potential Sources

of Information

Service level agreements and standards

to assess the third party’s performance and to confirm that

existing provisions continue to address risks and the bank’s

expectations.

Audited and other financial reports

to confirm the third party’s financial condition remains sound

and in compliance with contractual requirements.

Audits and reports to confirm the

third party’s compliance with all applicable laws and regulations.

Internal reports to review changes

in the bank’s risk assessment and supporting risk-management

processes.

The bank and third party’s

contingency testing results to evaluate the ability to respond to

and recover from service disruptions or degradations.

Review and testing of control effectiveness

to assess whether the third party’s control environment remains

sound, including SOC reports and self-assessments to industry standards.

Information security testing results

to assess the third party’s ability to maintain the confidentiality,

availability, and integrity of customer data (where applicable) and

the bank’s systems, information, and data.

Customer complaints to assess the

volume and subject matter of complaints and the timeliness and appropriateness

of the third party’s response to them.

Communication with the third party

to assess changes in key processes.

The third party’s staffing

and succession plans and organizational charts to assess changes in

the third party’s key personnel involved in the activity and

to determine whether key personnel have assumed responsibilities that

may detract from their ability to perform under the third party’s

agreement with the bank (e.g., affiliation with other entities).

Training materials provided to the

third party and bank staff for continued education.

Public filings, news articles, social

media, and customer feedback about experiences with the third party.

Example: Ongoing Monitoring

A community bank offers banking products and services

through a relationship with a nonbank third party. In this arrangement,

customers interact directly with the third party to access products

and services, such as opening and accessing deposit accounts, conducting

transactions, viewing account details, and receiving customer support.

The bank conducted a risk assessment during the planning

stage and identified multiple risks associated with this arrangement.

Consistent with the bank’s risk-management practices, bank management

conducts ongoing monitoring of third parties to ensure that the third

party continues to manage the risks and abide by contractual terms.

For illustrative purposes, this example only focuses on the bank’s ongoing monitoring activities related

to a limited set of AML/CFT as well as compliance and consumer protection

considerations:5

The third-party relationship may expose

the bank to increased risk of noncompliance with applicable AML/CFT

requirements in the areas of Customer Identification Program (CIP),

Customer Due Diligence (CDD), and suspicious activity monitoring if

the third party fails to meet its contractual or other obligations.

The third-party relationship may

expose the bank to increased risks of noncompliance with consumer

protection laws and regulations that may arise from the third party’s

disclosure of personal customer information, misrepresentations, or

misleading statements to customers about products or services, or

failure to comply with applicable dispute-resolution requirements.

Before entering the arrangement, the third party

undertook several remedial actions related to AML/CFT and consumer

protection compliance controls to help mitigate risks identified in

the bank’s risk assessment. These actions included strengthening

controls at the third party related to CIP and CDD requirements, suspicious

activity monitoring, providing required consumer disclosures, monitoring

of customer support interactions, and the handling of customer disputes.

The bank’s ongoing monitoring covers the full

range of risks associated with the arrangement. In particular, to

manage the identified risks noted above, bank management

maintains regular communications regarding

the third party’s risk-management practices, such as those related

to AML/CFT and consumer protection;

provides feedback on any changes

to the third-party’s risk-management practices that may impact

the bank’s compliance with applicable laws and regulations;

obtains and reviews copies of the

third party’s internal and external audit reports (independent

testing), compliance reviews, and other testing of internal controls.

This testing may include sampling the third party’s files related

to CIP information collected at account opening, documentation related

to ongoing CDD, and ongoing suspicious activity monitoring conducted

on behalf of the bank. This information may include transaction reviews,

escalations of potentially suspicious activity, and other documentation

related to compliance functions fulfilled by the third party;

confirms access to customer, transaction,

and monitoring information consistent with the contractual arrangement;

monitors the third party’s impact

on customers, including access to or use of consumer information,

the third party’s interaction with customers, handling of customer

complaints and inquiries, and communications with customers to ensure

accurate representation of the bank’s products and services;

and

maintains an effective compliance management

system (i.e., board and management oversight, policies and procedures,

training, monitoring, audit, and consumer complaint resolution process)

that addresses this and other third-party relationships, including

compliance with applicable consumer protection laws and regulations.

The examples are provided for illustrative

purposes, are not comprehensive, and will not be applicable to all

situations.

Termination

A community

bank may choose to end its relationship with a third party for a variety

of reasons. A bank typically considers the impact of a potential termination

during the planning stage of the life cycle. This consideration may

help to mitigate costs and disruptions caused by termination, particularly

for higher-risk activities, including critical activities.

TPRM Guidance

A banking

organization may terminate a relationship for various reasons, such

as expiration or breach of the contract, the third party’s failure

to comply with applicable laws or regulations, or a desire to seek

an alternate third party, bring the activity in-house, or discontinue

the activity. When this occurs, it is important for management to

terminate relationships in an efficient manner, whether the activities

are transitioned to another third party, brought in-house, or discontinued.

Potential

Considerations

How will the termination affect the

bank’s operations and its compliance with applicable laws and

regulations? Will any higher-risk activities, including critical activities,

be affected?

What are the financial implications

of terminating the relationship?

What alternative third parties are

available to which the bank can transition, or can the bank perform

the activity in-house?

How ready are bank staff, systems,

and control environments to move the outsourced activity in-house,

if needed?

How will the bank and the third party

handle intellectual property?

What access to bank systems or information

has the third party been granted? How and when will this access be

removed?

If the third party has access to

bank or customer data, when and how will the bank confirm that the

data has been returned or destroyed?

Will the bank have access to data

to meet its AML/CFT requirements and other recordkeeping obligations?

How will the bank manage risks associated

with the termination or migration, including the impact on customers?

What additional controls and processes

will the bank put in place during the transition?

Potential Sources

of Information

The bank’s contract with the

third party, to verify how parties may exit the relationship and the

conditions under which fees or penalties will be imposed for early

termination.

The bank’s budget to assess

the impact of costs and fees associated with termination.

Any outlines of steps or resources

that the bank had previously developed to support its exit from the

activity or to transition the activity to an alternative third party

or in-house.

Inventory of the bank or customers’

data at the third party to support risk management associated with

data retention and destruction, information system connections and

access control, or other control concerns.

Assessments of the bank’s systems,

processes, and human resources to determine whether the bank has the

capability, resources, and time to transition the activity to another

third party or bring the activity in-house with limited disruption

to the bank’s operations.

The bank’s third-party inventory

to assess existing relationships with other third parties to transition

the activity to them, if appropriate.

The bank’s considerations for

transitioning customer accounts with limited disruption to customers

and the bank’s operations.

Example: Termination

A community bank’s contract requires that the

third party receive approval before it uses a foreign-based subcontractor

to perform its obligations to the bank. As part of its ongoing monitoring

of the third-party relationship, the bank’s management discovers

that the third party has relied on a foreign-based subcontractor for

a higher-risk activity without informing the bank. The contract states

that the bank can terminate the relationship if the third party breaches

a requirement in the contract.

Management considers

terminating the relationship, as the third party has defaulted on

its contract with the bank by not obtaining approval for engaging

the foreign-based subcontractor. To facilitate the decision for termination,

management reassesses the relationship through the following practices:

Review of contract terms to confirm

the bank’s rights and options for termination, including notification

and timelines. Management also consults with its legal counsel to

determine whether early termination fees, penalties, or other restrictions

may apply;

Consultation with the bank’s

operations and compliance teams to determine the potential impact,

costs, and risks related to termination;

Assessment of potential operational,

compliance, and financial risks to transition to a new service provider;

Assessment of potential customer

impacts arising from termination and transition to a new service provider

and considers steps to mitigate them;

Evaluating whether the bank’s

risk-management practices are adequate and capable of managing the

risks anticipated from the termination of the contract and potential

transition of the activity to a new service provider; and

Reporting to the board of directors

on the potential risks of the termination. The report can include

management’s recommendations on legal, operational, and compliance

risks arising from termination and transition, including risk and

cost mitigation.

The examples are provided for illustrative

purposes, are not comprehensive, and will not be applicable to all

situations.

Governance

Community

banks typically consider the following governance practices throughout

the third-party relationship life cycle: oversight and accountability,

independent reviews, and documentation and reporting.

TPRM Guidance: Oversight and Accountability

A banking organization’s board of directors

has ultimate responsibility for providing oversight for third-party

risk management and holding management accountable. . . . A banking

organization’s management is responsible for developing and

implementing third-party risk management policies, procedures, and

practices, commensurate with the banking organization’s risk

appetite and the level of risk and complexity of its third-party relationships.

TPRM Guidance: Independent

Review

It is important for a banking organization

to conduct periodic independent reviews to assess the adequacy of

its third-party risk management processes. . . . A banking organization

may use the results of independent reviews to determine whether and

how to adjust its third-party risk management process, including its

policies, reporting, resources, expertise, and controls.

TPRM Guidance: Documentation

and Reporting

Documentation and reporting,

key elements that assist those within or outside the banking organization

who conduct control activities, will vary among banking organizations

depending on the risk and complexity of their third-party relationships.

Potential

Considerations

How do the bank’s policies and

procedures promote effective third-party risk-management governance?

How do documentation and reporting

enable the bank’s board of directors to consistently oversee

third-party risk management?

How does the bank’s board of

directors hold management accountable for third-party risk management?

Do the bank’s governance structure

and internal control environment effectively promote compliance with

bank policies and procedures and applicable laws and regulations?

Has the bank accurately assessed the

resources required (including level and expertise of staffing) to

manage third-party risks?

Does the bank effectively document

and maintain a current inventory of all third-party relationships

that clearly identifies those relationships associated with higher-risk

activities, including critical activities?

Has the bank effectively evaluated

the accuracy and timeliness of risk and performance reporting?

Has the bank effectively conducted

periodic independent reviews of the bank’s third-party risk

management?

When and how does the bank’s

management inform its board of directors about third-party risks?

Potential Sources

of Information

The bank’s strategic plan to

verify that the bank’s third-party risk-management practices

are aligned with its strategic objectives.

Applicable policies and procedures

to assess whether they address risks posed by third-party relationships.

The bank’s contingency testing

plans to understand how the bank maintains operations during disruptions.

Audit reports to assess the bank’s

risk management and pertinent internal controls.

The bank management’s periodic

reporting to the board of directors on third parties that support

higher-risk activities, including critical activities.

Documentation of the bank’s

actions to remedy material third-party issues, including performance

deterioration.

Other internal reports regarding

the bank’s third-party relationships.

AppendixGovernment Resources

for Community Banking Organizations’ Third‑Party Risk Management

These resources are not all inclusive, and other

sources of information may be available, particularly on specific

topics.

Federal Financial Institutions Examination

Council (FFIEC), “Joint Statement: Security in a Cloud Computing

Environment,” news release, April 30, 2020, https://www.ffiec.gov/press/pr043020.htm.

FFIEC, Bank Secrecy Act/Anti-Money

Laundering Examination Manual (Arlington: FFIEC, February 2015), https://bsaaml.ffiec.gov/manual.

See 12 U.S.C. § 1831p–1. The agencies

implemented section 1831p–1 by regulation through the “Interagency

Guidelines Establishing Standards for Safety and Soundness.”

See 12 C.F.R. pt. 30, appendix A (OCC), 12 C.F.R. pt. 208, appendix

D–1 (Board); and 12 C.F.R. pt. 364, appendix A (FDIC).

This example does not identify all potential third-party

risks posed by this relationship. Further, the actions noted are not

all-inclusive of ongoing monitoring actions that may be appropriate

to manage identified AML/CFT and consumer protection risks.